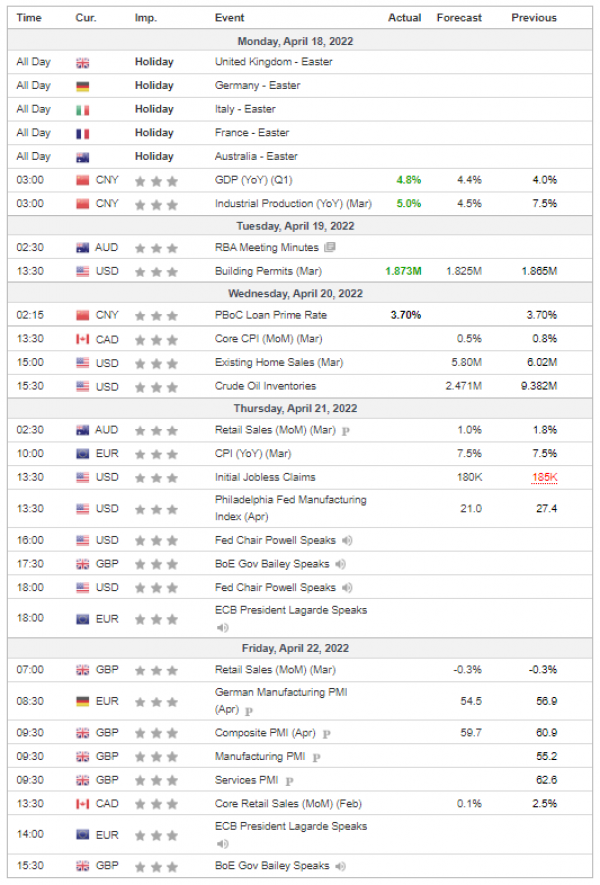

Rising US Treasury bond yields and the cautious market mood allowed the dollar to outperform its rivals last week. The euro continued to slide against the dollar remaining under bearish pressure. The embargo on Russian oil is still on table and the EU is planning to ban Russian oil in the coming weeks after the second round of French Presidential elections is over.

The British pound was little changed against the dollar. The UK's CPI for March reported last week rose 7% while forecast stood at 6.7%.

The Japanese yen continued to weaken and trades at its lowest level since May 2002. Japanese Finance Minister Suzuki commented on the yen devaluation saying that “yen's rapid weakening can have a negative impact but a weak yen is positive overall”. The benchmark 10-year US Treasury bond yield is currently around 2.9%.

Gold rose last week touching a fresh multi-week high near $2,000 on Monday on the back of safe-haven flows. Rising inflation across the world is pushing gold higher.

Last week, all major US stock indexes slid further. Negative for equities is the move in real yields, with the yield on the 10-year U.S. Treasury Inflation-Protected Securities approaching 0%. The earnings season is entering its second week and big investment banks such as Goldman Sachs reported mainly positive quarterly results. This week Tesla will post its results.

Oil prices rose last week. Traders fretted over tight global supplies after Libya halted some exports due to civil unrest and as factories in Shanghai prepared to reopen post a Covid-19 shutdown, easing some demand worries. The possibility of a European Union ban on Russian oil for its invasion of Ukraine continues to keep the market on edge as Russian forces launched their anticipated offensive in eastern Ukraine.